Hopefully, though not necessarily, we’re making more than minimum wage in our thirties. Whether you are or not, though, I hope you’d be interested in the statistic saying that the Federal minimum wage, adjusted for inflation, is worth less than it was 50 years ago. I find that to be an extremely sad statistic.

Someone asked on Quora (my absolute favor online pleasure site where I can get lost in questions and answers for hours) the other day: “How could 1950’s families afford to have only a working father, but a stay at home mother?” A bunch of people provided answers about eating out less and saving more, but one answerer got right to the point: Basically, when there was more productivity at a company in the 1950’s, the workers made more money. When there’s more productivity at a company now, the top 1% keep excess money, and the workers never see it.

In 1950, the average income per year was $3,210. Since the minimum wage was $0.75 an hour (on January 25, 1950), people working the minimum wage the average number of hours a week (43) made $1,677 a year. So, by working the average number of hours and making the federal minimum wage, you could make 52% of the average wage. In 1950, a new house cost $8,450. So, if you never spent a penny of the money you earned, it would take roughly 5 years at the federal minimum wage to save the amount equal to that of a new house.

In 2015, the average income per year was $55,775. Since the minimum wage in 2015 was $7.25 an hour, people working the minimum wage the average number of hours a week (34) made $12,818 a year. So, by working the average number of hours and making the federal minimum wage, you could make 23% of the average wage. The average sale price for a new house in January 2016 was $365,600. So, if you never spent a penny of the money you earned, it would take 29 years at the federal minimum wage to save the amount equal to that of a new house. Do those seem equal to you?

Also, according to the EPI: “Between 1973 and 2014 productivity grew 72.2 percent…while the typical worker’s compensation was nearly stagnant…9.2 percent over the entire 1973–2014 period. This allowed a huge concentration of wealth at the highest 1% of people.”

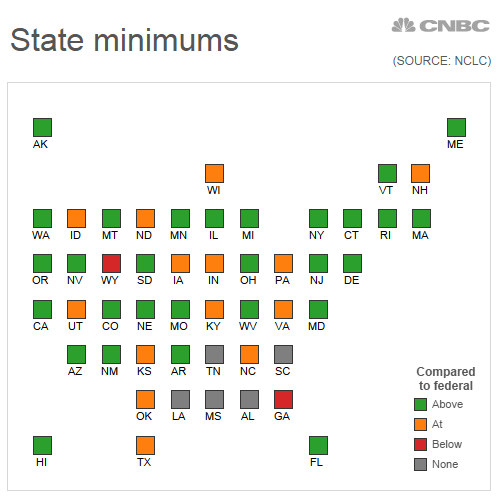

So what can we do about this? Well, California and New York have increased their minimum wages (with the exclusion of certain small businesses) to $15/hr and that will go into effect by 2022 and 2018, respectively. This is great progress. Because, according to a study by the Center for American Federal minimum wage: “the minimum wage should have hit $21.72 an hour if it kept up with worker productivity.” Even if minimum wage kept up with inflation alone, the study goes on to say, federal minimum wage should at least be $10.52 an hour.

Even if you’re not politically active, and don’t want to get into debates about the minimum wage, you might feel some anger over this the same way I do. People can’t live on the federal minimum wage as it stands…and even if they can live a scraped together life, it doesn’t help the economy anyway that people living on an ‘unlivable’ federal minimum wage have barely any buying power.

What can we do? At the very least, it’s good to be aware of this issue, and spread the word when we can. It’s not true that people in the 1950’s simply “saved more.” I’m a huge fan of saving but don’t let yourself get gaslighted by minimum wage excuses like that one. There are americans who work the maximum number of hours allowed a week, and save as much as they can, who are still simply unable to make enough money to live on. This is a problem for us all.

")