Jane wrote an article about the Slash Generation over a year ago- Are We the Slash Generation?– and it’s one of our most read articles. Why? Well, beside’s Jane’s captivating writing skills, I’m convinced this interest in the slash generation prevails because the slash generation is ubiquitous and is already bleeding into future generations.

What is the slash generation? It’s a generation of 20 and 30 somethings that have multiple jobs and even multiple full time careers. For example: Actor/Yoga Teacher/Nutritionist/Graphic Designer, or DJ/Cafe Owner/Artist/programmer. We all have hobbies, such as occasional running or painting, but the slash generation has multiple JOBS. I’m a prime example of slash generation- my job title is presenter/product specialist/ demonstrator/ marketer/ writer/ actor/ director/ producer. I’m probably forgetting something.

Why is the slash generation on the rise? Well, the economic landscape is changing for millennials in their twenties and thirties- and the changes are affecting younger and older generations as well. Jobs that include pensions are now few and far between and companies don’t necessarily encourage employees to stick around. Changing jobs has become as frequent as changing your socks.

And there are good reasons to change jobs: minimum wage salaries don’t nearly keep up with inflation, most employers don’t reward you for sticking around, benefits are few and far between. So instead of sticking with one company, millennials are going wide and both starting their own companies and working with multiple employers on both a freelance and employee basis. Honestly, we sometimes need to do all these things to pay our bills.

The slash generation is a double edged sword: it can be very helpful to have multiple jobs and skills and to ‘go wide’ so that you have security if certain jobs don’t work out. But the slash generation is also sign of unfair economic times in America- where you can work very hard within companies and still not see anywhere near the kind of money you deserve. This is an era where companies can have spectacular financial success with their employees barely seeing a dime of that growth.

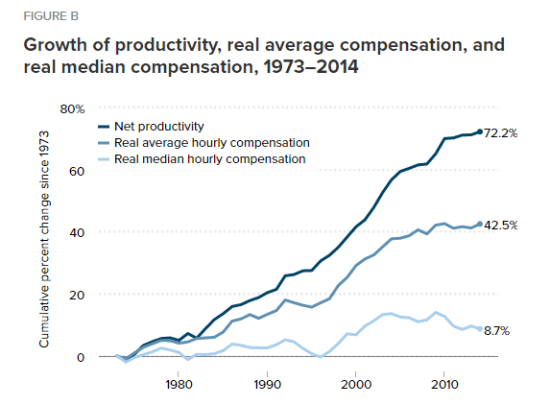

In America, there has been a 72.2% rise in productivity since 1973 and only an 8.7% rise in pay rate